Anyone who prepares Form 1120 but does not charge the corporation should not complete that section. Generally, anyone who is paid to prepare the return must sign and complete the section. However, a corporation with a fiscal tax year ending June 30 must file by the 15th day of the 3rd month after the end of its tax year. A corporation with a short tax year ending anytime in June will be treated as if the short year ended on June 30, and must file by the 15th day of the 3rd month after the end of its tax year. The corporation can view, print, or download all of the forms and publications it may need on IRS.gov/FormsPubs. Otherwise, the corporation can go to IRS.gov/OrderForms to place an order and have forms mailed to it.

Tax planning & preparation

Gross receipts include the aggregate gross receipts from all persons treated as a single employer, such as a controlled group of corporations, commonly controlled partnerships, or proprietorships, and affiliated service groups. See section 448(c) and the Instructions for Form 8990 for additional information. Certain real property trades or businesses and farming businesses qualify to make an election not to limit business interest expense. Also, you are not entitled to the special depreciation allowance for that property.

Forms & Instructions

To keep close track of your expenses and profits and to make better-informed business decisions, you may wish to utilize accounting software like FreshBooks. Click here for a free trial or to get started on creating your own account. The safest and easiest way to receive a tax refund is to e-file and choose nol carryover worksheet excel direct deposit, which securely and electronically transfers your refund directly into your financial account. Direct deposit also avoids the possibility that your check could be lost, stolen, destroyed, or returned undeliverable to the IRS. Eight in 10 taxpayers use direct deposit to receive their refunds.

Access additional help, including our tax experts

To learn more about the information the corporation will need to provide to its financial institution to make a same-day wire payment, go to IRS.gov/SameDayWire. Corporations must use electronic funds transfer to make all federal tax deposits (such as deposits of employment, excise, and corporate income tax). Generally, electronic funds transfers are made using the Electronic Federal Tax Payment System (EFTPS). However, if the corporation does not want to use EFTPS, it can arrange for its tax professional, financial institution, payroll service, or other trusted third party to make deposits on its behalf. Also, it may arrange for its financial institution to submit a same-day payment (discussed below) on its behalf. EFTPS is a free service provided by the Department of the Treasury.

Disclose information for each reportable transaction in which the corporation participated. Form 8886, Reportable Transaction Disclosure Statement, must be filed for each tax year that the federal income tax liability of the corporation is affected by its participation in the transaction. A corporation must figure its taxable income on the basis of a tax year. A tax year is the annual accounting period a corporation uses to keep its records and report its income and expenses.

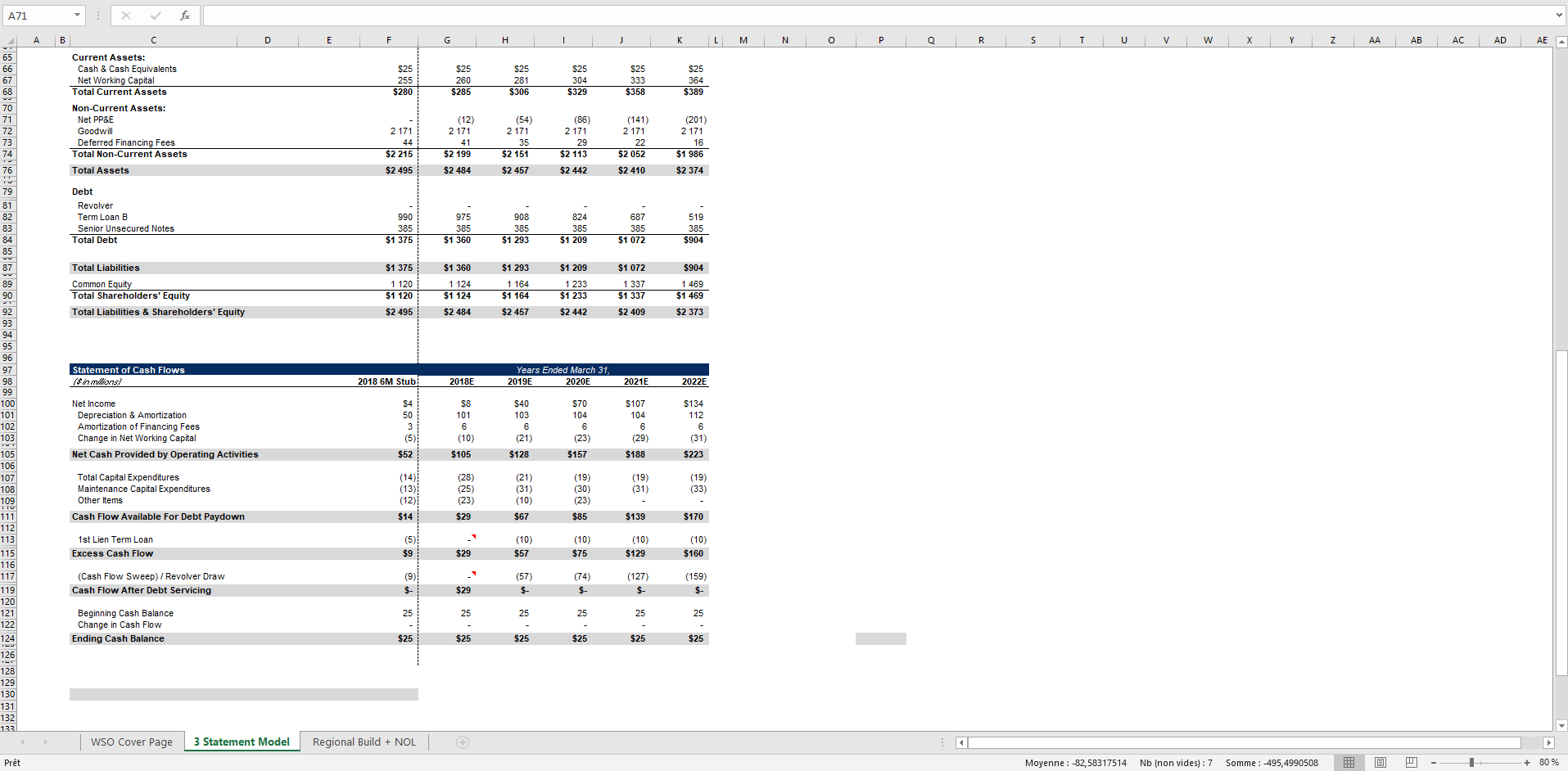

How a Net Operating Loss (NOL) Works

This statement must show that you are choosing to waive the entire carryback period for the current year NOL under section 172(b)(3) of the Internal Revenue Code. With TaxAct you are able to electronically file your return and include this statement. However, section 267A does not apply if a de minimis exception is satisfied.

- For details, see the instructions for Form 1045 or Form 1040-X..

- For more information on reporting the deferred tax and interest, see the Instructions for Form 8621.

- 4134, Low Income Taxpayer Clinic List, at IRS.gov/pub/irs-pdf/p4134.pdf.

- Corporations may be required to adjust deductions for depletion of iron ore and coal, intangible drilling and exploration and development costs, certain deductions for financial institutions, and the amortizable basis of pollution control facilities.

The Coronavirus Aid, Relief, and Economic Security (CARES) Act suspended the changes made by the TCJA for tax years 2018, 2019, and 2020; however, the new rules apply for 2021 and onward. The net operating loss can generally be used to offset a company’s tax payments in other tax periods through an Internal Revenue Service (IRS) tax provision called a loss carryforward. This offers a benefit to a company in that it can reduce a company’s future tax liability by offsetting taxable income in future years.

The trust fund recovery penalty may be imposed on all persons who are determined by the IRS to have been responsible for collecting, accounting for, or paying over these taxes, and who acted willfully in not doing so. The penalty is equal to the full amount of the unpaid trust fund tax. 51 (Circular A), Agricultural Employer’s Tax Guide, for details, including the definition of responsible persons. Applicable entities and electing taxpayers can elect to treat certain credits as elective payments.

If the corporation is attaching Form 8996, check the “Yes” box for question 25. On the line following the dollar sign, enter the amount from Form 8996, line 15. Attach Schedule UTP to the corporation’s income tax return. A taxpayer that files a protective Form 1120 must also file Schedule UTP if it satisfies the requirements set forth above. If the partnership agreement does not express the partner’s share of profit, loss, and capital as fixed percentages, use a reasonable method in arriving at the percentage items for the purposes of completing question 5b.

Deixe um comentário